Last month the RSA released a proposal for a Universal Basic Opportunity Fund (UBOF) which they propose as a test case for a Universal Basic Income (UBI) in the UK. As the idea of some kind of universal cash distribution has entered the lexicon of policy discourse in recent years, particularly spurred by the unknown effects of automation and the known impending rise in our elder population, this report provides a useful mannequin to review how well the idea of a UBI fits our predicament. There are undoubtedly trends towards greater economic insecurity for many in the developed countries, with associated ructions in politics, which make a better safety net an important focus for research, and that has led to renewed interest in the basic income idea.

The premise of UBI is that there are sufficient resources available to make a universal and unconditional payment to all citizens, and that the result of that distribution will be enhanced freedom, opportunity and wellbeing. The context is that all sorts of previously reliable characteristics of the labour market have fallen away, like long term jobs, consistent hours, adequate or better pay, and collective bargaining, only to be replaced with low pay, inconsistent terms, and unreliable tenure. And many of these factors look like they will only get worse as we head into the next stage of automation powered by “artificial intelligence” which is likely to affect the middle-skilled as well as the low-skilled. The interest in a basic income stems as much from these anxieties as it does from an interest in reform.

A short version of this full length review is on the RSA site.

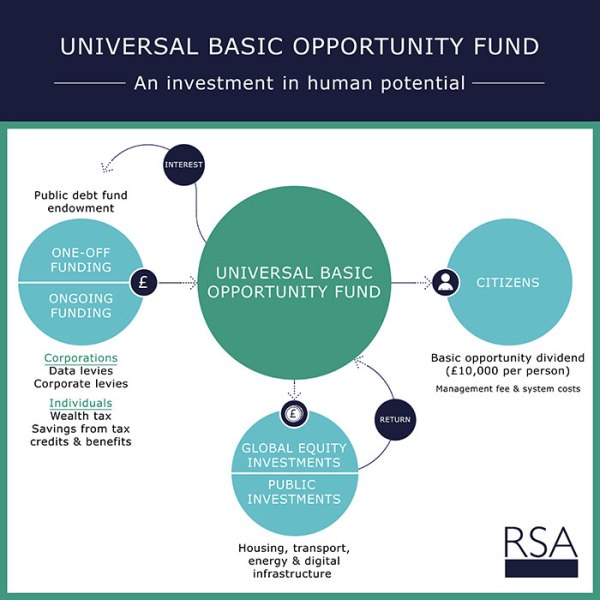

As UBI advocates have been quick to point out: the UBOF is not a UBI, despite the report being titled “Pathways to Basic Income”. The RSA do assert that their UBOF idea could be used to evaluate aspects of how a UBI could work and because it aims towards that goal it incorporates many aspects that are common to UBI proposals, providing us with an opportunity to look at the idea of UBI in the round. The report frames a proposal for a £10,000 grant that would allow people under 55 years old to make changes to their lives. The headlines ([https://www.theguardian.com/society/2018/feb/16/tax-amazon-facebook-and-apple-more-for-uk-universal-pay-study]) trailed the report as using a tax on major social media and tech companies to pay for a universal basic income, in reality the report only mentions “data levies” as a possible source of revenue to bolster a proposed sovereign wealth fund.

Like most UBI-type proposals, the primary aim of the UBOF is to increase autonomy and agency in the lives of citizens. To wit it lists “Greater Freedom” as the first of its Anticipated Benefits, followed by “Opportunity to change path” in second, and “Better health and wellbeing” in third place. The primary focus of the UBOF is enabling “people to take risks they would not otherwise take”, and to do so in a way that prioritises personal “choices best aligned with their needs” as reference to the idea that individuals make better choices for themselves than an overarching state. A section linking low pay and insecurity with health and wellbeing is extensive and well referenced, establishing that the long term removal of insecurity will result in better health outcomes.

This gives us insight into the driving motivations of many who support UBI in principle: they see UBI as a way to empower individuals, freeing them from the bureaucracy and oversight of state apparatuses. This intention is supported by two essential aspects of faithful UBI proposals, that the payments be unconditional and unwithdrawable. To understand UBI you have to absorb this strong attachment to freeing the individual from the state, born of both the experience of conditional welfare programs in the West, and the communist past in the East. In this way UBI proposals mirror the post-industrial conception of the individual person as distinct from their society — an idea reflected in contemporary conceptions of the “consumer economy”, and in the individual “rational actor” models of neo-liberal economic theory.

Unconditionality

To align with that individually orientated worldview is it essential that the universal component of UBI means universally _individual_, applying to all individuals as solo entities. This is the essential freedom that UBI promises, and which requires that any proposal must accrue its benefits to every person equally and outside the review of any external institution. This is a utopian notion of humanity which sits uncomfortably with the social structure within which a UBI is developed in practice, leading to the many difficulties and contortions exhibited in real world attempts to nurture UBI out of the incubator and into life. The RSA’s UBOF report provides us with a useful example to examine how these arise and allows us to look at whether these are simply details of implementation that can be tweaked to fit with the principles, or unresolvable contradictions.

The central tenets of unconditionality and non-withdrawal appear to be early casualties of attempts to develop real world, rather than theoretical, proposals for UBI. And the UBOF proposal is a case in point: while application to the program is supposedly unconditional, it is age limited (only people under 55), time limited (only 2 years in a 10 year program), subject to application to and approval by an authorised institution (all of whom will be “subject to a code of conduct”), and requires “labelling” of the proposed purpose that the money will be used for. In the RSA’s 2015 more general UBI proposal they suggest that recipients “will have to identify five witnesses, including two non-immediate family members, to support them”. In this year’s election in Italy, the 5 Star Movement’s proposed UBI would be withdrawn if three job offers are rejected.

Why is it that these core principles, that are the defining features of UBI, find it so hard to make their way past the first post and into proposals for implementation? Is it because UBI is a system of redistribution that is tapping a source of funds that is universal in the sense that it is social and shared, but is delivered in the most fungible method possible to meet the objective of freeing the individual from their society?

Where UBI proposals are funded from socially external sources, such as resource surpluses like the Alaska oil fund, conditionality is much less likely to feature in the implementations, which suggests that the society’s perspective on whether what is being distributed is sourced from other citizens, or at the communal expense of other citizens, affects the degree to which conditionality is politically necessary for a UBI proposal to gain popular acceptance. In Thomas Paine’s proposal for a universal distribution, which is a commonly adopted source of inspiration for many in the UBI camp, he was proposing the fair and equitable distribution of the fruits of Nature. But since 1796 much of the “the earth itself” has become social property and the fruits of its exploitation generally do flow into the coffers of society in some form of fees or taxes levied by the government on the exploiters, such as oil companies and cell service providers. In today’s world it is generally true that the fruits of Nature are already being captured and already being put to use as common assets of the society and it is only when there is an enormous surplus from geological luck, such as in the major oil producing countries, that people sometimes conceive of those funds as outside the bounds of social assets. Once a natural resource is adopted as a social asset, as oil is in Norway, it is integrated and deployed like every other social asset towards common social need, and not a individual entitlement. Further complicating this issue in the 21st century is the growing recognition of natural liabilities, such as pollution and climate instability, which cannot be allocated universally or individually and will require collective social action to pay off. Reversing this historical trend towards conceptualising Nature’s bounty as a social asset would seem to be both difficult and a prerequisite for its distribution to be seen to be free of social conditionality.

Then there’s the issue of distributing cash. The conditionality of the existing welfare systems is a core driver behind the desire of UBI proponents to move away from just such a system, but if it is the case that the reason those welfare programs are so conditional is exactly because they dispense cash, and that we all have an innate understanding of the fungibility of cash, then perhaps cash and conditionality can not be separated in the human mind and therefore cannot be separated in policies that apply to human societies. The dependency link between conditionality and cash may be anecdotal but it is nevertheless inescapable that conditional cash distribution is a widespread feature of modern societies, and the unconditional distribution of cash is as rare as hen’s teeth. Not to extrapolate from this that it is the normal propensity of humans to see cash as a reward, not a right, would be churlish.

These problems with conditionality surface in other of aspects of the UBOF proposal as well. In the case of higher rate tax payers there is a suggestion that the grant should instead become a loan to avoid dishing out free money to people who don’t need it. The UBOF also allows people to use their grant to fund the start up of a business, but then alludes to mechanisms to prevent people just banking the money and using it to invest in the stock market. How the state would distinguish between startup and investment activities is elusive, but it is the fact that there is a desire to try to allow one thing and not the other that points again to the difficulty of proposing the direct distribution of cash, and is obviously something the report’s authors are alive to.

It’s easy to see the alignment of UBI’s aspiration to free individuals from their society with the distribution of cash to each individual unconditionally, but what is difficult to imagine is any resources that do not have social connections in the first place. Even resources which arise from the bounty of Nature have evident alternative uses as communal assets. Add to that the psychological difficulties inherent in cash distribution and it’s not hard to see why implementations of UBI quickly get caught up in a tangle of superficial unconditionality but detailed conditionality.

Stepping outside the UBI worldview for a moment, there are many who would find the attachment to seeing the individual as separate from society as ridiculous. After all, how can one conceive of our species as anything other than a group species in which every individual is completely dependent on their group for their material safety, mental sanity, and ultimate satisfaction? In the thousands of years over which our species evolved the cohesion of our social groups was based on the mutual exchange of services. “No man is an island” has been part of English literature for almost 400 years, and perhaps before that was unworthy of written statement as it was such a fundamental assumption. Nevertheless the nature of the lived experience, seeing as we do out from inside our skulls at the rest of the world as if we are separate from it, and exaggerated by the move to large scale, urban societies as we pass through the industrial-technical-information revolutions, has led to mass assimilation of the notion of individualism, however ridiculous it may be.

What does a significant UBI cost?

Large sums of money are inevitably involved when proposing to distribute significant sums of cash to every member of a society. The top line numbers for a full UBI in the UK are measured in the hundreds of billions, and the relatively small “pilot” UBOF proposal doesn’t disappoint in this area either. The full UBOF program costs £462 billion over 10 years, providing applicants £5,000 a year for 2 years for themselves and their dependents. That’s in line with other proposals and suggests that paying everyone in the UK about 25% of the national average wage would cost around £200 billion a year. That’s double total NHS spending, or a quarter of total public spending, or 10% of GDP.

Because a UBI is cash it is nearly always envisaged as counting as income to the recipient, and therefore subject to tax. This results in the large amount of “churn” that is also a common aspect of UBI proposals, in which much of the money distributed as the UBI is then withdrawn through the tax system. Illustrative of this “churn” phenomena, the UBOF proposal would retrieve £187 billion of the headline cost through adjusting the taxes of participants to remove their annual Personal Allowance, thus withdrawing immediately £2,300 of the headline £5,000 distribution from anyone earning the national average (£23,000) while receiving UBOF, and withdrawing all of the UBOF value for anyone earning £36,500 or more. Through this give-and-take the UBOF reduces its headline cost to the public purse from £462 billion to £275 billion.

Withdrawing tax allowances would still leave the UBOF distributing cash to people who are also receiving traditional, conditional cash benefits, so to avoid doing that the report removes various of those cash benefits from applicants during their program participation. This is also a common and natural feature of UBI proposals, after all the intention is to move away from conditional systems. But this is also where another crack appears because it is very hard to remove all conditional benefits without disadvantaging the most needy. So, like many other UBI proposals, the UBOF only removes some benefits and leaves others in place resulting in a system that remains reliant on conditionality to retain fairness.

Taking away some benefits saves another £86 billion which are then replaced by a portion of the UBOF grant equivalent to the value of their previous benefit entitlements. This would have a variable impact on program participants depending on how many benefits they previously qualified for, but most of the reduction comes from withheld Child Benefit which as worth £800 a year per child on average (£1,600 for a family with 1.8 children), meaning that the UBOF would be worth £4,200 per dependent child. Withdrawing Job Seekers Allowance would leave an unemployed person with only £1,200 a year extra on UBOF, which is a curious choice given the goal of helping people make changes in their lives and speaks to the difficult trade offs inherent in designing cash distribution programs in societies that already practice conditional benefits.

Thus we arrive at the final, post-churn, headline number of £188 billion. Over the extended 13 year timeframe (including an 3 year introductory period during which admission would be by lottery to allow the supporting administration to come up to speed) this is what yields the advertised £14 billion a year cost. However it must be noted that using that number ignores the fact that taxes have already been increased by the same amount. If we use the UBOF to provide a guide to what an equivalent UBI would cost we would have to use the 10 year program length divided by the 20% participation rate (2 years out of 10, per person) which comes to £188 billion **a year** (£94.5Bn plus £93.5Bn in taxes).

As you may have noticed above, it can be hard to pin down what to use as the “cost” of a UBI. Is it the headline number? Is it the tax adjusted number? I think, honestly, you have to use the headline number because then you separate the UBI from the potential sources of funding. The tax adjusted number just incorporates a particular scheme designer’s predilection for a specific means of meeting the costs. And then there’s the difficulty of pinning down the other side of the equation: the value to recipients. As soon you start adjusting the tax system to help pay for the UBI you change the net value of the UBI to recipients. All this means that a conclusive answer to the affordability question is elusive, depending as it does on so many variables in the construction of both the UBI itself and the mechanisms used to fund it. “Good and careful implementation is key”, is noted by Anthony Painter, one of the UBOF report’s authors, and we can see just how important the details are when the results and effects can vary so widely with a constant UBI value but differences in funding.

Is £188Bn affordable? While “affordability” gets sceptical reception in economist circles, it has clear comprehension in lay parlance: the availability of funds from a reasonable tax. Most people would say that £188Bn was not affordable as it would require raising an additional 9% of GDP in taxes. £188 billion is equivalent to the elimination of the personal allowance twice over, which means about £400 a month for most tax payers and is the same as the value of the UBI.

This is a normal result a UBI funded from income taxes, and it’s inevitable if you’re going to balance a cash distribution with income taxes, which is why pretty much every UBI proposal ends up sourcing funds external to the income tax system in order to sustain a notion of actually delivering a distribution of extra income. The UBOF does this too, and uses another common mechanism of other UBI proposals: the “sovereign wealth fund”.

Magic Money

The example in the UBOF report is a useful guide to some of the mechanisms that many UBI proponents are thinking about, including wealth taxes, sovereign debt, financial investments, and other new taxes such as on “data” in the RSA’s UBOF report.

A decade or so ago “sovereign wealth funds” were hardly mentioned but since the major petro-nations started putting their surpluses to work in the financial markets, and after those same funds became part of the rescue packages after the last financial crash, it seems that everyone wants one of their own. The trouble is that there’s a world of difference between having a massively positive balance of payments because you are selling the oil under your ground, and not. If the UK had started a sovereign wealth fund when there was lots of North Sea oil to be had that would be one thing, but the idea that we can start a fund by printing the money and lending it to ourselves, which is what the RSA report suggests, and just deciding to call it “sovereign wealth” is another thing all together. At its most simplistic it is mortgaging the future to play the stock market today — a text book definition of “financialisation”.

To entertain the idea that playing the stock market with public debt is an proper function for government betrays a mindset captured by the 20th century’s delusion that money represents everything that can be represented, and is at the same time simply a technical invention of our modern cleverness. In fact money is a deeply unconscious metaphor at the heart of social cohesion, and to play loose with it is to play loose with the binds that tie a society together and prevent it from unravelling into a Mad Maxian anarchy of distrust. There’s a good argument to be made that both Trump and Brexit descend directly from the QE (aka money printing) deployed to save our financial system over the last decade. The willingness to create debt for one reason and not for another suggests that we are not all playing on a level field, and that some people’s problems are subject to different rules than other people’s. As an example, here’s a below-the-line comment on a major news site in response to a story about global interest rates rising and the end of ‘cheap money’, and it represents a widely held view: “Unless you knew the right people, in which case it wasn’t ‘cheap’ money, it was Free money”. This is a pernicious erosion of the trust that underpins not just the financial system, but our democracy as well.

The credibility of money goes far beyond the technical credibility of a currency in relation to other currencies, into the realm of a stabilising constant around which all members of a society can orientate themselves and accept the relative differences in outcomes that are manifestations of chance beyond the desires or hopes of any individual. Money is nothing less than a substitute, and a much preferable one, for violence as one of two central, organising constants for a human society — the other is the rule of law. In our modern, advanced societies monetary credibility and the rule of law are our Maypole and the ribbons are our democracy. Without the pole there are only ropes dividing people, where before there was structure that all accepted.

The primary issue with these new monetary ideas is that they conceptualise a society as the child of its economy when the reality is exactly the opposite. They make the government dependent on systems that government is supposed to either be independent of or in control of: financialisation and monetary credibility. Ultimately a government must be a structure for human society that is independent of the vagaries of the market and will provide solidity even when markets collapse or fail. And if the nation has its own currency then the government is also charged with responsibility for maintaining the credibility of that currency, not for the sake of the currency itself but for the good of the society. It may do so at arms length through an independent central bank but that bank derives its authority from the government, and it is the government that retains ultimate responsibility. Just because a sovereign can print money, doesn’t mean that doing so doesn’t have consequences. If money can be printed for one thing, then why not another, and why not more?

There is only a small step from the lunacy of public debt as public wealth to the pure fantasies of other “modern monetary theories”. In these more obscure theories the identity of money is completely severed from its social nature and conceptualised only as if it is some transitory thought flitting across the mind of an absent professor. Central to these more outlandish theories is the mantra that “money is debt” and that sovereign currency issuers are both creditor and debtor in any debt issuance, leading to some version of a proposal in which sufficient money is printed to meet need and any associated debt is voided. This is a vision of human society without its Maypole in which, somehow, a shared delusion of the continuing existence of a phantom Maypole provides ongoing orientation for everyone. It’s a classic case of _assumptive delusion_ in which the background state of affairs is assumed to have permanence because the observer takes it for granted.

You can’t have a sovereign wealth fund if you’ve got no wealth to put in it, and even if you did put something in it the idea that playing with public, social capital on financial markets is an even remotely sensible idea is bonkers. If there is even the slightest need remaining unfilled or possible investment in productivity unmade back in the real world of your society that would be the best use of available funds. If any society has truly reached such a point that they have so much and nothing better to do with it than to invest in financial markets, then something or someone is being exploited somewhere. One wonders how much wealth would be left in the petro-nations’ wealth funds after back payment of carbon taxes.

So if a sovereign wealth fund is tricky, how about some other new kinds of tax? The UBOF report suggests some wealth taxes and a new tax on “data”. Also popular more broadly are the Tobin tax on financial transactions and a growing interest in the idea of taxing robots. All share in common a desire to find sources of revenues to fund public goods, to balance the contributions of capital and labour, and perfectly worthwhile endeavours those are. However trouble arises whenever a single tax is considered in isolation, because in the end every tax adds to cost in the economy generally, and we need to pay attention to the overall effect of all the taxes in aggregate. We can inject some sobriety into this debate by looking at the total share of GDP that any society can reasonably expect to raise in taxes, irrespective the specific type of taxation considered. The average of the highest taxing 25 OECD countries is 42%, which is also the average of the tax take of the EA-19. Very few countries take more than 45% in tax and in those countries, for example France at 45%, one can observe some discomfort with their fiscal positioning. It seems a reasonable extrapolation that there is a natural boundary above which productivity declines and/or tax evasion increases, and that that level is somewhere visibly short of half of total output. Dozens of countries experimenting in quite different circumstances, over considerable periods of time, with different political structures and changing political orientations, are unlikely to have landed so closely together without there being larger forces at work in the subconscious of human societies. That this macro analysis mirrors the micro experience of taxation of personal pay, whereby the prospect of paying a majority in tax reduces incentive and increases the desire to cheat to a greater degree than the payment of a minority, adds weight to this mean.

So even if we do need to move towards the taxation of new or different sectors of our economy, that does not mean that there will be much more money available. The UK’s tax take is around 38% of GDP and spending is at 41%, so there may be another few percent available and the mix of sources could well change, but the notion that another 10% (£200Bn) is available from any source should be treated with a great deal of scepticism. There’s certainly no evidence in the real world that tax rates 10% above where we have them already are feasible or sustainable. We should also bear in mind here that the UBI we have been considering thus far is only a quarter of the national average wage: £5,000. There are those who advocate starting with a low UBI and gradually increasing it to approximate the average wage, and that would require something close to the total of all current public spending.

Priorities

Ultimately the function of government is to allocate available social resources to the maximum benefit of society, working from a list of priorities derived from an understanding of the requirements necessary to enable human communities to thrive. It is generally acknowledged that first and foremost amongst those priorities is the security of the population, envisaged initially as the security from violence and then the basic material safety of each person. This progresses to enabling opportunity through public education and health. Condensed and economically vibrant societies benefit greatly from public transport and access to communications systems, and in a democracy the ability of citizens to participate necessitates access to the output of a free press as well as hybrid fabric of institutions to enable distributed decision making. The provision and maintenance of these public goods, which are primarily services, is uncontroversially the priority role of government. Most UBI supporters accept this description of the role of government, and envisage UBI providing a layer of emancipating personal freedom on top of this set of universal basic services. There are more libertarian-minded UBI supporters on the other side of the Atlantic who see UBI as a substitute for many of these public services, but that approach does not get much traction elsewhere.

Given this acceptance of the priorities for social resources we should examine what level of service is appropriate in a developed society, and what the cost of delivering those services is before we can know what additional resources might be available after those have been satisfied. This is the greatest challenge that UBI faces in the real world: when there is so much need for basic services (like housing, healthcare, education, nutrition and transport) any proposal to allocate cash directly to individuals comes into direct competition with those public services. As one UBI advocate put it: basic service funding is “dangerous” because it soaks up the available fiscal space and will not leave enough room for a meaningful UBI.

Best use of resources?

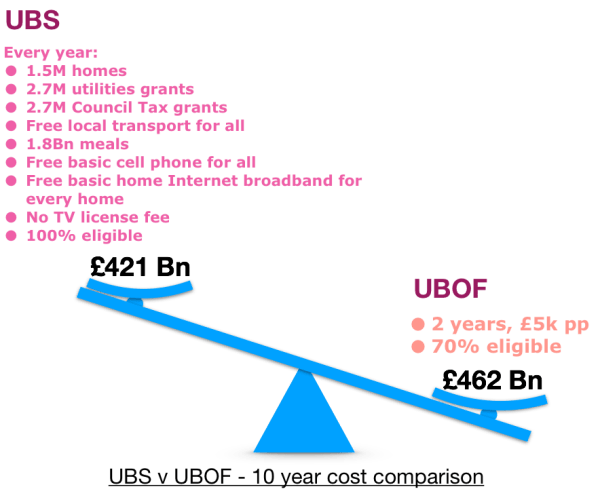

The Institute of Global Prosperity at UCL recently modelled a dramatic expansion of free public services to see what they would cost, and this provides a useful comparison in weighing the value of a UBI. (Full disclosure: I am part of the team at the IGP involved in this work.) The IGP report assessed the cost of their Universal Basic Services (UBS) at £42.2Bn a year, which would provide 1.5 million new social housing units, 2.7 million Council Tax and utility grants, feed the food insecure population with 1.8 billion meals a year, give everyone free local transport services, and free basic cell phone and Internet access as well as covering the cost of the TV license fee. That’s an awful lot of services, and they would dramatically reduce the cost of living, by 80%, for those on the lowest incomes that used the services. The existence of those services would increase economic security for the whole population, just by the very fact of their accessibility in the event of need – like the NHS.

Weighed against a total program cost for UBOF of £46Bn a year, let alone a full UBI at £95Bn, it’s arguable that the UBS proposal would increase the economic security of more people with less conditionality than the UBOF. It would certainly build more social capital, and provide more flexible support than the UBOF as it would not be time limited. And this is the problem that UBI proposals always come up against: there are better and more effective uses of the public’s taxes than universal cash distribution. To be fair to European-style supporters of UBI, unlike their American compadres, they do not think that public services should be reduced to fund their UBI programs, and therein lies the rub. If public services are funded as a priority because they deliver more security for the same spend, then there is little money left for cash distribution on top of that. Taxes need to go up in the UK just to meet the inadequate level of existing public spending and a fully operational UBS program as outlined by the IGP would require 2.3% more in taxes, taking the UK tax take to around 43% of GDP. Given what we know about typical tax takes of the highest taxing countries in the world, that’s pretty close to the top tax burden that is sustainable in a free and democratic country. The notion that the UK public would be prepared to raise taxes even higher than that to fund a cash distribution is not really a credible proposition. The UK has only ever had tax takes of 45%+ during world wars, and briefly after the 1970’s “oil shock”.

Economic security

Creating “economic security” drives much of the RSA’s justification for UBI and UBOF, which they define as “The degree of confidence that a person can have in maintaining a decent quality of life, now and in the future, given their economic and financial circumstances.” The goals of reducing fear and increasing everyone’s sense of safety in their community are undoubtedly key to liberating the full potential of our societies, and are objectives shared by all who are looking at different ways to build more cohesive, productive, and sustainable futures. But a sense of security is derived from much more than a bank balance, it is also reliant on the solidity of the social infrastructure within which we live, the fabric of institutions and facilities that are bigger than us as individuals and which give us confidence that we will not fall below a certain floor whatever the outcomes of chance or our individual choices. So while there is little doubt that increasing economic security is key to a peaceful and successful future for UK society, that does not lead straight to the door of cash distribution as the solution. Proper security is based on the reliable availability of support and tangible social fabric, whether it is accessed or not, which together create a greater degree of confidence than personal money ever can.

The UBOF report defends UBI by claiming that its critics “are unable to take into account the impact of UBI on economic security and the consequent behavioural effects of such impacts” and that the critics do “not consider the behavioural impacts and long-term consequences of targeting and conditionality”. But neither can this report. Some of the institutions, OECD and IMF, that have examined the possible implementation of a UBI and concluded that it is very expensive and increases poverty are mentioned in the report, and there are others closer to home, such as IPR, JRF and LSE reports, which reach similar conclusions.

Conclusion

UBI has not had a trouble-free birth in its modern incarnation, and the UBOF report offers us some insight into the difficulties and complications. It seems that UBI has more credibility as an idea than a policy. In practice it is stuck between a fierce competition for available tax revenues and a libertarian fantasy to abolish the social state. The former looks very difficult, and no one sensible wants the latter. If UBI cannot compete successfully against basic public services for a large share of the fiscal pie, and if the fiscal pie cannot be grown much above where it is today through either adventurous monetarism or new taxes, then UBI proposals will always be smaller than would be necessary to achieve their transformational ideals.

The premise of UBI is that there are sufficient resources available to make a universal and unconditional payment to all citizens, and that the result of that distribution will be enhanced freedom, opportunity and wellbeing. But the availability of sufficient resources is unproven, and the lives of ordinary citizens can be greatly enhanced for a fraction of the cost by increasing the provision of access to free basic services.

The idea of a UBI has value if it brings you to a place where you can conceptualise the benefit of every member of your society accessing at least some basic share of the prosperity of your society. But as a practical policy that can be delivered in reality it has thus far proved of little value, and to the extent that it remains a distraction for those whose talents we all need deployed on the great search for a sustainable and peaceful future, then perhaps it is UBI that is truly the most “dangerous” idea of our times.